ARM Holdings — The Company Inside Every Smartphone

ARM Holdings (Nasdaq: ARM) is a British semiconductor and software design company headquartered in Cambridge, United Kingdom. Founded in 1990, ARM creates processor instruction set architectures (ISAs) and microprocessor designs that it licenses to semiconductor companies worldwide. ARM does not manufacture chips — instead, companies like Apple, Qualcomm, Samsung, NVIDIA, and Amazon pay ARM licensing fees and royalties to use its designs. This "fabless IP" model makes ARM the most widely used processor architecture in history. ARM's designs power virtually every smartphone, most tablets, an increasing share of laptops and servers, automotive systems, smart TVs, wearables, and an enormous range of IoT devices. The global semiconductor industry that ARM operates within is tracked in our global company valuations analysis.

- Full name: Arm Holdings plc · Nasdaq ticker: ARM · Listed September 14, 2023

- Headquarters: Cambridge Science Park, Cambridge, UK · Major offices in San Jose, Austin, Munich, Tokyo, Bengaluru, Shanghai

- Business model: Pure IP licensing · No chip manufacturing · Revenue from licensing fees + royalties per chip shipped

- Architecture: ARM ISA (Instruction Set Architecture) · Current: ARMv9 · Previous dominant: ARMv8

- Key products: Cortex-A (application processors) · Cortex-M (microcontrollers) · Cortex-R (real-time) · Mali/Immortalis GPU IP · Ethos NPU (AI)

- Ownership: SoftBank Group ~90% · Public float ~10% · No single large public institutional shareholder

ARM Holdings Revenue — Financial Performance FY2019 to FY2026E

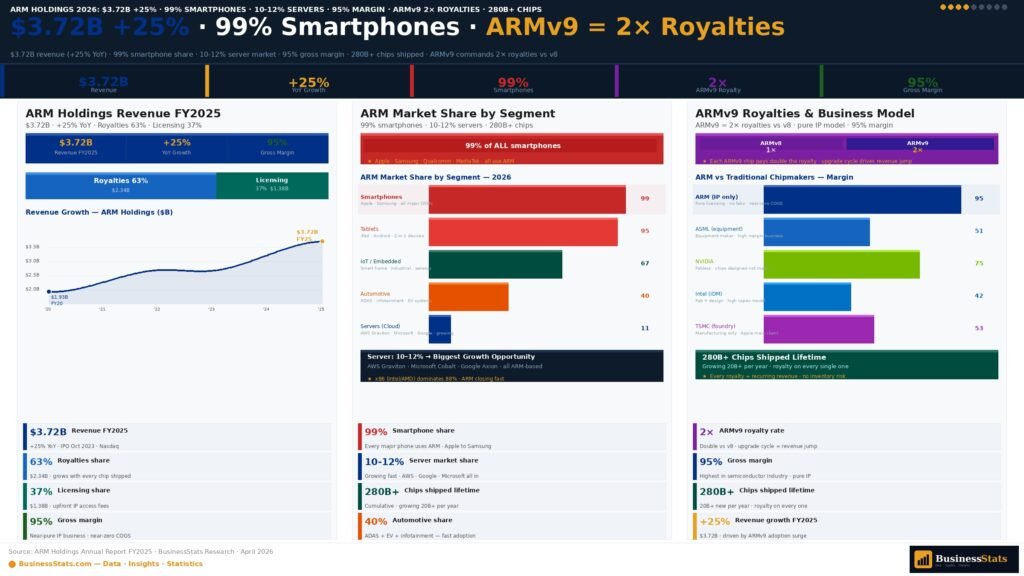

ARM's financial year ends in March. FY2025 (ended March 2025) revenue was approximately $3.72 billion, representing approximately 25% growth year-on-year and approximately 40% growth over two years. ARM's revenue has two distinct streams: Royalty revenue (ongoing per-chip payments, approximately 60–65% of total) and Licensing revenue (upfront payments for IP access, approximately 35–40%). The key growth driver is the transition from ARMv8 to ARMv9 architecture, which commands approximately 2× the royalty rate — as more chips transition to v9, ARM's revenue per chip shipped rises significantly. The broader economic context is analyzed in our global GDP analysis.

Revenue Breakdown — Royalties vs Licensing

- Royalty revenue FY2025: ~$2.35B (63% of total) · per-chip payments from licensees · grows with chip shipments + v9 transition

- License revenue FY2025: ~$1.37B (37% of total) · upfront fees for IP access · large deals can cause quarterly volatility

- Gross margin: ~95% · one of the highest in all of technology · no manufacturing cost of goods

- Operating margin FY2025: ~30–35% · lower due to heavy R&D investment (~40% of revenue)

- R&D spend FY2025: ~$1.5B · critical investment maintaining technology leadership

- Free cash flow FY2025: ~$1.7B · strong cash generation despite R&D intensity

ARM Architecture Market Share — Smartphones, Tablets, Servers & IoT

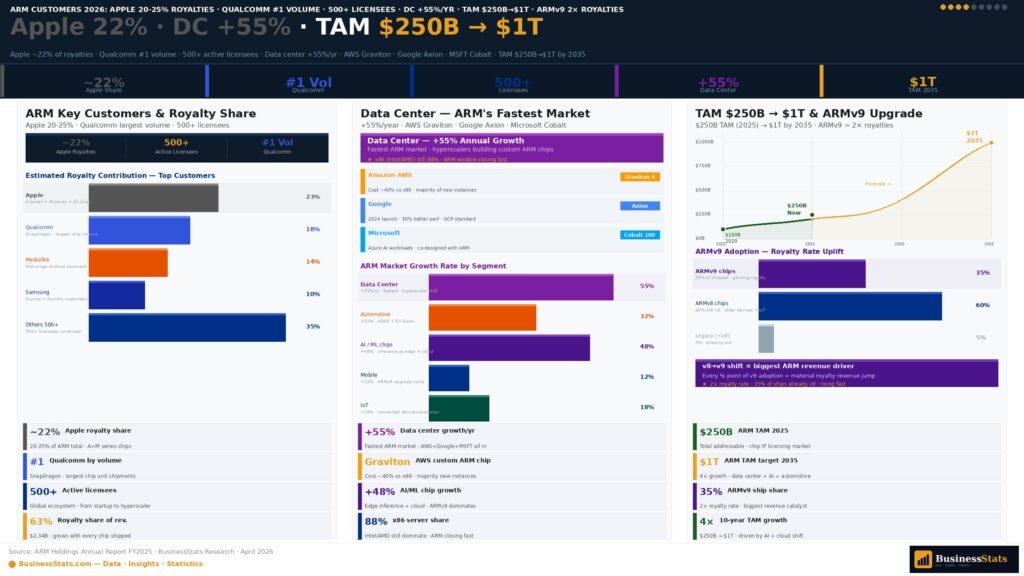

ARM's market dominance in mobile computing is near-total — approximately 99% of all smartphones globally use ARM-based processors. The company's expansion into data centres represents its most significant growth opportunity. Amazon, Google, Microsoft, and Apple have all designed custom ARM-based server chips, moving away from x86 (Intel/AMD) for selected workloads. ARM-based server chips now hold approximately 10–12% of the global server processor market — up from near zero in 2018. The competitive dynamics between ARM, x86, and the emerging RISC-V architecture are critical to understanding ARM's long-term position. The broader competitive landscape is tracked alongside global consumer technology in our Amazon statistics and social media technology analysis.

- Smartphones: ~99% · Apple (A/M-series), Qualcomm (Snapdragon), Samsung (Exynos), MediaTek — all ARM-based

- Tablets: ~99% · iPad (Apple Silicon), Android tablets (Qualcomm/MediaTek), Samsung Galaxy Tab

- Laptops: ~30%+ and growing · Apple MacBook (M1/M2/M3/M4 chips) + Windows on ARM (Snapdragon X)

- Servers/Cloud: ~10–12% · AWS Graviton, Google Axion, Microsoft Cobalt, Apple M-series Mac servers

- Automotive: ~40–45% · growing fast as vehicles become computers · ADAS, infotainment, EV battery management

- IoT/Embedded: ~65–70% · Cortex-M dominates microcontroller market · billions of smart devices

- Wearables: ~95% · Apple Watch, Samsung Galaxy Watch, Fitbit — virtually all ARM

ARM Holdings' Key Customers — Apple, Qualcomm, NVIDIA & More

ARM's customer base spans virtually every major semiconductor and consumer electronics company in the world. Over 500 companies hold active ARM architecture licenses. The largest customers by revenue contribution are Apple (architectural licensee — designs fully custom ARM chips), Qualcomm (largest royalty payer by volume), Samsung (both Exynos chips and foundry services), MediaTek (dominant in mid-range Android), and NVIDIA (Grace data center CPU). A critical new development is the rise of hyperscaler custom chips — Amazon, Google, Microsoft, and Apple all designing their own ARM-based server chips, bypassing Intel and AMD. This trend is transforming the data center landscape and represents ARM's largest growth opportunity over the next decade. The global consumer platforms that deploy ARM-based devices are tracked in our Amazon statistics and retail e-commerce data.

- Apple: Architectural license (custom A/M-series chips) · ~20–25% of ARM royalty revenue · ~230–250M iPhones/year + MacBooks + iPads + Apple Watch

- Qualcomm: Largest volume royalty payer · Snapdragon chips in majority of premium Android phones · ongoing legal disputes with ARM over custom CPU designs

- MediaTek: #1 by smartphone chip volume globally · dominant in mid-range Android · ~36% global smartphone chip market share

- Samsung: Exynos chips (consumer devices) + foundry manufacturing of ARM-based chips for others

- NVIDIA: Grace CPU (data center) · Orin and Thor (automotive/autonomous vehicles) · critical partnership for AI era

- Amazon AWS: Graviton chips (Graviton3, Graviton4) power AWS cloud infrastructure · reportedly 20%+ of AWS compute now ARM

- Google: Axion CPU (data center) · Tensor chips (Pixel phones) · both custom ARM designs

- Microsoft: Cobalt CPU (Azure cloud) · Windows on ARM (Snapdragon X) · Surface Pro X

ARM Holdings and Qualcomm are locked in a landmark legal dispute that could reshape the semiconductor licensing industry. The core issue: Qualcomm acquired Nuvia (a chip design startup) in 2021 for $1.4 billion. Nuvia held an ARM architectural license that allowed it to design custom ARM CPUs. ARM claims that when Qualcomm acquired Nuvia, the license did not automatically transfer — meaning Qualcomm's new Snapdragon X Elite chips (designed using Nuvia's CPU cores, now called Oryon) were built on unlicensed ARM architecture. ARM filed suit in 2022 seeking to cancel Qualcomm's architectural license entirely. If ARM wins and cancels Qualcomm's license, it could be catastrophic for Qualcomm — but also disruptive to the broader ARM ecosystem. The case went to trial in late 2024. The outcome will set critical precedent for how architectural licenses transfer through M&A in the semiconductor industry. This dispute is tracked alongside the broader UK tech landscape in our UK tech companies analysis.

ARM Holdings History — From Acorn Computers to $110 Billion

ARM's journey from a small Cambridge joint venture to the world's most important semiconductor IP company spans 35 years and includes some of the most consequential decisions in technology history — including an early partnership with Apple that would eventually make ARM the architecture inside every iPhone. The history of ARM is inseparable from the history of mobile computing. The history of ARM mirrors the history of mobile computing — context tracked in our Instagram statistics and YouTube analysis.

ARM Holdings — Target Markets, Chip Shipments & Growth Outlook

ARM estimates its total addressable market (TAM) at approximately $250 billion by 2025, growing to approximately $1 trillion by 2035. The growth is driven by three major structural shifts: the expansion of ARM-based chips into data centres (where x86 has historically dominated), the proliferation of computing in automotive systems as vehicles become computers, and the explosion of AI edge computing where energy efficiency makes ARM uniquely competitive. ARM's chip shipment data — tracking chips shipped by all licensees — provides the most comprehensive view of ARM's market penetration. The economic implications of ARM's dominant position in the AI era are analyzed in our global GDP analysis and wealth and technology investment data.

| Segment | Annual Shipments | ARM Market Share | Growth Rate | ARM TAM | Key Players |

|---|---|---|---|---|---|

| Smartphones | ~1.4B chips | ~99% | +5% | ~$20B | Apple, Qualcomm, MediaTek, Samsung |

| IoT / Embedded | ~9.0B chips | ~65% | +12% | ~$45B | NXP, STMicro, TI, Microchip |

| Networking / Infra | ~2.0B chips | ~40% | +15% | ~$20B | Marvell, Broadcom, Qualcomm Infra |

| Consumer Electronics | ~2.5B chips | ~85% | +4% | ~$15B | Samsung, MediaTek, Realtek |

| Automotive | ~450M chips | ~45% | +22% | ~$30B+ | NVIDIA Orin/Thor, NXP, Renesas |

| Data Center / Cloud | ~150M chips | ~10–12% | +55% | ~$35B+ | AWS Graviton, Google Axion, MS Cobalt |

| Laptops / PCs | ~90M chips | ~30% | +25% | ~$10B | Apple Silicon, Snapdragon X |

| Wearables | ~500M chips | ~95% | +8% | ~$5B | Apple Watch, Samsung, Fitbit |

- Total chip shipments FY2025: ~16–17 billion ARM-based chips per year · ~280B cumulative since founding

- Fastest growing segment: Data center (+55%/year) · ARM going from 0% to 10%+ of server market in 7 years

- Largest by volume: IoT/Embedded (~9B chips/year) · Cortex-M dominates microcontroller market globally

- Highest royalty rate: Data center and smartphones (v9 architecture commands premium pricing)

- v9 transition progress: ~25% of royalty revenue from v9 in FY2025 · projected 50%+ by FY2027

- TAM 2025: ~$250B · TAM 2035E: ~$1T (ARM's own estimate) · AI, automotive, data center driving expansion

ARM Holdings — Revenue Forecast & Growth Outlook 2026–2030

ARM's financial outlook is among the most compelling in the global semiconductor industry. Three structural tailwinds are converging simultaneously: the v9 architecture transition (doubling royalty rates per chip), the data center expansion (ARM going from 0% to a projected 25%+ of server chips by 2030), and the automotive revolution (every new vehicle requires more computing power). Analyst consensus projects ARM revenue reaching approximately $4.3–4.5 billion in FY2026 and potentially $7–10 billion by FY2030. The long-term thesis: ARM earns more per chip AND more chips are shipped every year across more categories. The global technology investment context is covered in our financial markets analysis and wealth and investment data.

| Fiscal Year | Revenue (Est.) | YoY Growth | Royalty Rev. | v9 Share | Server Share | Key Driver |

|---|---|---|---|---|---|---|

| FY2025 (actual) | $3.72B | +25% | ~$2.35B | ~25% | ~10–12% | v9 early adoption |

| FY2026E | ~$4.3–4.5B | +16–21% | ~$2.8B | ~35% | ~14% | v9 scale-up, AI servers |

| FY2027E | ~$5.0–5.5B | +16–22% | ~$3.4B | ~50%+ | ~18% | v9 majority, data center |

| FY2028E | ~$6.0–7.0B | +18–27% | ~$4.2B | ~65% | ~22% | Automotive ramp-up |

| FY2029E | ~$7.5–8.5B | +15–25% | ~$5.2B | ~75% | ~25% | AI edge + auto |

| FY2030E | ~$9–11B | +15–25% | ~$6.5B | ~80%+ | ~28% | TAM $1T convergence |

- v9 royalty double effect: As v9 chips replace v8, ARM earns approximately 2× more per chip shipped — even without volume growth, revenue rises substantially

- Data center acceleration: Server chips growing +55%/year · AWS Graviton4, Google Axion, Microsoft Cobalt, Apple M-series servers — each new product family adds recurring royalties

- Automotive megatrend: By 2030, every new vehicle globally is projected to contain 15–20 ARM-based chips across ADAS, infotainment, EV management, and connectivity — up from 5–8 today

- AI edge computing: On-device AI (smartphones, laptops, wearables) requires more powerful chips — accelerating v9/v10 adoption and increasing royalty per device

- IoT volume growth: Connected devices projected to reach 75 billion by 2025 (Statista) — majority ARM-based — providing a long-term volume floor

- v10 architecture (2025+): ARM's next-generation architecture expected to command even higher royalty rates — extending the royalty step-up thesis beyond v9

Bull case ($150–200B market cap by 2030): ARM achieves 25%+ server market share, v9/v10 royalty step-up drives revenue to $10B+, automotive royalties ramp faster than expected, SoftBank reduces stake creating more free float and institutional buying. AI inference boom drives unprecedented chip volume. ARM becomes the dominant architecture for the AI era across every device category. Bear case ($50–70B by 2030): RISC-V adoption accelerates in IoT, cutting ARM's lowest-margin volume; Qualcomm wins its legal battle over architectural license terms, setting precedents reducing ARM's negotiating leverage; data center ARM adoption plateaus as Intel/AMD defend server turf aggressively; and SoftBank selling creates persistent share overhang. Base case (~$120–150B): Steady execution of the v9 transition, gradual data center share gains, strong automotive royalties. ARM remains the world's most important chip IP company regardless of scenario. The competitive dynamics are tracked in our digital technology statistics.

ARM Holdings — Key Statistics & Facts 2026

Frequently Asked Questions — ARM Holdings 2026

ARM Holdings reported total revenue of approximately $3.72 billion in fiscal year 2025 (ending March 2025), up approximately 25% from $3.0 billion in FY2024. Revenue consists of two streams: Royalty revenue (~$2.35B, 63% of total) — ongoing per-chip payments from licensees; and Licensing revenue (~$1.37B, 37%) — upfront fees for IP access. The key growth driver is the transition to ARMv9 architecture, which commands approximately 2× the royalty rate of v8. FY2026 analyst consensus is approximately $4.3–4.5 billion.

ARM Holdings has a market capitalisation of approximately $100–120 billion in early 2026, making it the UK's largest technology company by market cap and one of the most valuable semiconductor companies globally. ARM re-listed on Nasdaq (ticker: ARM) in September 2023 at $51 per share, valuing it at approximately $65 billion at IPO. The stock traded as high as approximately $180 in 2024. SoftBank retains approximately 90% of ARM's shares, making the effective free float relatively small.

Approximately 99% of all smartphones globally use processors based on ARM architecture. This includes Apple iPhones (A-series and M-series, custom ARM designs), all Samsung Galaxy phones (Qualcomm Snapdragon or Samsung Exynos — both ARM-based), and virtually all Android devices using Qualcomm, MediaTek, or Samsung processors. ARM does not manufacture chips — it licenses its processor designs to chip companies, which pay ARM a royalty for each chip sold. Over 280 billion ARM-based chips have been shipped cumulatively.

ARM's largest customers include: Apple (architectural license for custom A/M-series chips, ~20–25% of royalties), Qualcomm (largest royalty volume payer, Snapdragon chips), MediaTek (dominant mid-range Android, ~36% global smartphone chip share), Samsung (Exynos chips + foundry), NVIDIA (Grace CPU, automotive chips), Amazon AWS (Graviton data center chips), Google (Axion CPU + Tensor chips), and Microsoft (Cobalt CPU). Over 500 companies hold active ARM licenses.

ARM operates a pure intellectual property (IP) licensing business model. ARM designs processor architectures but does not manufacture any chips. Revenue comes from: (1) Licensing fees — upfront payments when companies license ARM's instruction set architecture or processor designs; (2) Royalties — ongoing payments (typically 1–2% of chip selling price) for every ARM-based chip shipped. This model delivers approximately 95% gross margins — one of the highest in all of technology — and means ARM earns from virtually every smartphone, laptop, server, and IoT device shipped globally.

ARM Holdings completed its Nasdaq IPO on September 14, 2023, listing at $51 per share under the ticker 'ARM'. The IPO raised approximately $4.87 billion — the largest technology IPO of 2023. At the IPO price, ARM was valued at approximately $54.5 billion. The IPO was oversubscribed approximately 10×. SoftBank retained approximately 90% of shares. ARM had previously been dual-listed on the London Stock Exchange and Nasdaq before SoftBank's $32 billion acquisition in 2016. The NVIDIA acquisition attempt (2020–2022) was blocked by regulators before the 2023 IPO.

ARM Holdings employs approximately 6,500–7,000 people globally as of 2025. Headquarters: Cambridge, UK. Major offices: San Jose (California), Austin (Texas), Munich (Germany), Tokyo (Japan), Bengaluru (India), Shanghai (China). Approximately 40% of ARM's workforce is in the UK, making it one of the UK's largest tech employers by revenue-per-employee. Staff are primarily semiconductor engineers, computer architects, software developers, and IP licensing specialists.

SoftBank Group retains approximately 90% of ARM Holdings' shares as of early 2026, following the September 2023 Nasdaq IPO in which only ~10% of shares were sold publicly. SoftBank acquired ARM in September 2016 for approximately $32 billion — the largest-ever acquisition of a European technology company at that time. SoftBank's stake in ARM is now worth approximately $90–100 billion, making it SoftBank's most valuable single asset and the primary driver of SoftBank Group's overall net asset value.

ARM estimates its total addressable market (TAM) at approximately $250 billion by 2025, growing to approximately $1 trillion by 2035. Key opportunities: Data Center/Cloud (~$35B+, growing +55%/year), Automotive (~$30B+, +22%/year), IoT (~$45B), Smartphones (~$20B), Laptops/PCs (~$10B), Networking (~$20B). The data center and automotive segments represent ARM's most significant growth opportunities, with hyperscaler custom ARM chips (AWS Graviton, Google Axion, Microsoft Cobalt) now powering significant AI and cloud workloads.

Apple holds an architectural license from ARM — meaning Apple licenses ARM's instruction set architecture (ISA) and designs fully custom processors (A-series for iPhone/iPad, M-series for Mac) rather than using off-the-shelf ARM designs. Apple pays ARM a royalty on every chip shipped. The exact rate is confidential. Given Apple ships approximately 230–250 million iPhones annually plus hundreds of millions of iPads, Macs, Apple Watches, and AirPods (all ARM-based), Apple likely accounts for approximately 20–25% of ARM's total royalty revenue — making Apple ARM's most strategically important customer.

ARMv9 (launched 2021) is ARM's biggest financial catalyst. v9 commands approximately 2× the royalty rate of the previous v8 architecture. As chip manufacturers transition from v8 to v9, ARM's revenue per chip shipped rises substantially without needing more chips to be sold. In FY2025, approximately 25% of ARM's royalty revenue came from v9-based chips, up from near zero in 2022. ARM projects v9 to represent the majority of royalties by FY2027–28. v9 features: enhanced AI capabilities (SVE2), improved security (Confidential Compute Architecture), better performance per watt, and mandatory security features for enterprise deployments.

Yes, ARM Holdings is profitable. FY2025: operating income approximately $1.2 billion; net income approximately $1.5 billion (benefiting from SoftBank-era deferred revenue). Gross margin: approximately 95% — one of the highest in technology. Operating margin: approximately 30–35%, lower due to significant R&D investment (~$1.5B/year, ~40% of revenue). Free cash flow: approximately $1.7 billion in FY2025. ARM's profitability is expected to grow significantly as v9 royalties scale and data center wins add high-margin revenue.

ARM is increasingly central to the AI chip ecosystem. NVIDIA's Grace CPU (data center AI) is ARM-based. Apple's M-series (with Neural Engine for on-device AI) are ARM-based. Amazon Graviton, Google Axion, Microsoft Cobalt — all custom ARM data center chips powering AI inference — run on ARM. ARM's Ethos NPU (Neural Processing Unit) IP is licensed to chip companies for on-device AI. The AI boom is a structural tailwind for ARM because AI requires more powerful, efficient chips — which drives faster v9 adoption and higher royalties, particularly in the data center market where ARM is growing fastest.

SoftBank acquired ARM Holdings in September 2016 for approximately £24.3 billion ($32 billion) — the largest acquisition of a European technology company ever at that time. The deal was completed just six weeks after the Brexit referendum. SoftBank's founder Masayoshi Son flew to the UK and personally negotiated with PM Theresa May, framing it as a vote of confidence in post-Brexit Britain. ARM was delisted from both LSE and Nasdaq. SoftBank later attempted to sell ARM to NVIDIA for $40 billion in 2020, but the deal was blocked by US, UK, EU, and Chinese regulators in 2022 over competition concerns. ARM then re-listed on Nasdaq in September 2023.

The three major processor architectures each have different competitive positions: ARM dominates mobile (99% smartphones), is growing rapidly in data centers and laptops, and is the clear leader for new computing categories (IoT, automotive, wearables). x86 (Intel/AMD) retains dominance in traditional PC and server markets (~88% of servers) but is losing share in data centers to ARM at the margin. RISC-V is an open-source alternative gaining traction in IoT, embedded, and academic settings — it is a long-term competitive threat to ARM in lower-margin segments but is not yet competitive in high-performance computing. Most analysts expect ARM to continue gaining data center and laptop share while RISC-V grows slowly in embedded markets.

Supporting: IDC — Worldwide Semiconductor Applications Forecaster · Market share by processor architecture and segment

Supporting: Gartner Semiconductor Research · Server processor market share · PC processor market data