UK Tech Industry — $1 Trillion Ecosystem, Europe's Largest

The United Kingdom's technology sector is the 3rd largest in the world, behind only the United States and China. With a total ecosystem value of approximately $1 trillion, the UK has built a tech industry that generates approximately £150 billion ($190B) annually — approximately 7.7% of total UK GDP. The sector employs approximately 3 million people directly, representing about 9% of the total UK workforce, with average salaries approximately 40% above the national average at approximately £55,000 per year. The UK's position as a global tech leader is backed by world-class universities (Oxford, Cambridge, Imperial, UCL), deep capital markets, English language advantage, and a strong legal framework for intellectual property. The broader context of UK economic strength is tracked in our global GDP analysis and financial markets report.

- Global ranking: #3 tech ecosystem globally (USA, China, UK) — ahead of Germany (#5), France (#6), India (#4)

- European leadership: UK has more unicorns, more VC investment, and more tech employment than any other European country

- Digital economy: UK digital economy worth approximately £150B/year — 7.7% of GDP

- Tech exports: UK tech services exports approximately £60B annually — a major driver of the UK's services trade surplus

- R&D investment: UK tech sector spends approximately £22B annually on R&D — among the highest R&D-to-revenue ratios globally

- Government support: UK AI Opportunities Action Plan (2025) committed £14B in private investment; National Quantum Strategy aims for 10% of global quantum market by 2033

Largest UK Tech Companies — Ranked by Valuation & Revenue 2026

The UK tech landscape spans publicly listed giants, private unicorns, and global subsidiaries. ARM Holdings — headquartered in Cambridge — is the UK's largest tech company by market capitalisation at approximately $100 billion+, despite being listed on Nasdaq rather than the London Stock Exchange. Among truly private UK startups, Revolut leads at approximately $45 billion, making it not just the UK's most valuable startup but one of the most valuable fintech companies globally. The global competitive context of these companies is tracked in our global company valuations analysis.

| Rank | Company | Sector | Valuation / Mkt Cap | Status | HQ | Founded |

|---|---|---|---|---|---|---|

| 1 | ARM Holdings | Semiconductors/IP | ~$110B | Nasdaq (2023) | Cambridge | 1990 |

| 2 | Revolut | Fintech / Neo-bank | ~$45B | Private | London | 2015 |

| 3 | Checkout.com | Payments | ~$11B | Private | London | 2012 |

| 4 | Wise (TransferWise) | Fintech | ~$9B | LSE (2021) | London | 2011 |

| 5 | Snyk | Cybersecurity/DevOps | ~$7.4B | Private | London | 2015 |

| 6 | Sage Group | Enterprise Software | ~£12B | LSE (FTSE 100) | Newcastle | 1981 |

| 7 | Octopus Energy | Energy Tech | ~$5B | Private | London | 2016 |

| 8 | Monzo | Fintech / Neo-bank | ~$5B | Private | London | 2015 |

| 9 | Darktrace | AI Cybersecurity | ~£3B | LSE (2021) | Cambridge | 2013 |

| 10 | OakNorth | Fintech / Lending | ~$2.8B | Private | London | 2015 |

| 11 | Starling Bank | Fintech / Neo-bank | ~$3.3B | Private | London | 2014 |

| 12 | Graphcore | AI Chips | ~$2.77B | Private | Bristol | 2016 |

| 13 | Softcat | IT Infrastructure | ~£3.5B | LSE | Marlow | 1993 |

| 14 | Wayve | Autonomous Vehicles/AI | ~$1B+ | Private | London | 2017 |

| 15 | Kainos Group | Digital Services | ~£1B | LSE | Belfast | 1986 |

| 16 | Cleo | AI Finance App | ~$1.6B | Private | London | 2016 |

| 17 | Computacenter | IT Services | ~£3B | LSE | Hatfield | 1981 |

| 18 | Thought Machine | Banking Tech | ~$2.7B | Private | London | 2014 |

| 19 | Featurespace | AI / Fraud Detection | ~$1B | Private | Cambridge | 2008 |

| 20 | Zopa | Fintech / Banking | ~$1B | Private | London | 2005 |

UK Tech Unicorns — 100+ Companies Valued at $1 Billion+

The United Kingdom has approximately 100–110 technology unicorns — private companies valued at $1 billion or more — making it the 3rd largest unicorn ecosystem globally after the USA and China, and the largest in Europe by a significant margin. London alone accounts for approximately 85–90 of these unicorns. The fintech sector dominates, accounting for approximately 30% of all UK unicorns. The concentration of UK unicorns in fintech reflects the combination of London's established financial services ecosystem, regulatory innovation (the FCA sandbox), and deep talent pools. The global unicorn and startup ecosystem is analyzed in our global company valuations report and consumer platform data in our Amazon statistics.

Revolut — founded in London in 2015 by Nik Storonsky and Vlad Yatsenko — is the UK's most valuable private technology company at approximately $45 billion, following its 2024 funding round. This valuation places Revolut above many established FTSE 100 companies by market capitalisation. Revolut has grown from a simple currency exchange card into a full financial super-app offering banking, cryptocurrency trading, stock investing, travel insurance, and business accounts. It serves approximately 50+ million customers across 35+ countries. Despite its valuation, Revolut only received its full UK banking licence in July 2024 — a milestone years in the making. The global digital payments landscape that Revolut competes in is tracked in our retail and payments analysis.

UK Tech Sector Breakdown — Fintech, AI, Cybersecurity & More

The UK's technology ecosystem spans a diverse range of sub-sectors, with fintech the undisputed leader by investment and company count. Artificial intelligence is the fastest-growing sector by investment. Cybersecurity is a structural growth area driven by rising enterprise demand globally. The UK's gaming industry — birthplace of Grand Theft Auto, Tomb Raider, and Elite — remains the largest in Europe. The social media landscape that UK tech companies participate in and market through is tracked in our social media statistics, Instagram analysis, and YouTube report.

- Fintech (~$8–10B VC/year): Revolut, Wise, Monzo, Starling, Checkout.com, OakNorth — UK is #2 globally after USA · £11B revenue · 76,000 employees

- AI and ML (~$6–8B): DeepMind (Alphabet), Wayve, Stability AI, Graphcore, PolyAI, Cleo — UK has 3rd highest AI research output globally

- Cybersecurity (~$2–3B): Darktrace, Snyk, Sophos, BAE Systems Applied Intelligence — global demand growing 15%/year

- SaaS/Enterprise (~$3B): Sage (FTSE 100), Kainos, Temenos UK, Thought Machine — strong B2B software heritage

- Gaming (~£3.4B revenue): Rockstar (GTA), Codemasters (F1), Frontier (Planet Coaster), Jagex (RuneScape) — largest gaming industry in Europe

- GreenTech/CleanTech (~$3B+): Octopus Energy ($5B), Bulb, Ripple Energy — UK's fastest growing tech sector 2024/25

- HealthTech (~$2B): Featurespace, Babylon Health, AI diagnostics companies — accelerated by NHS data partnerships

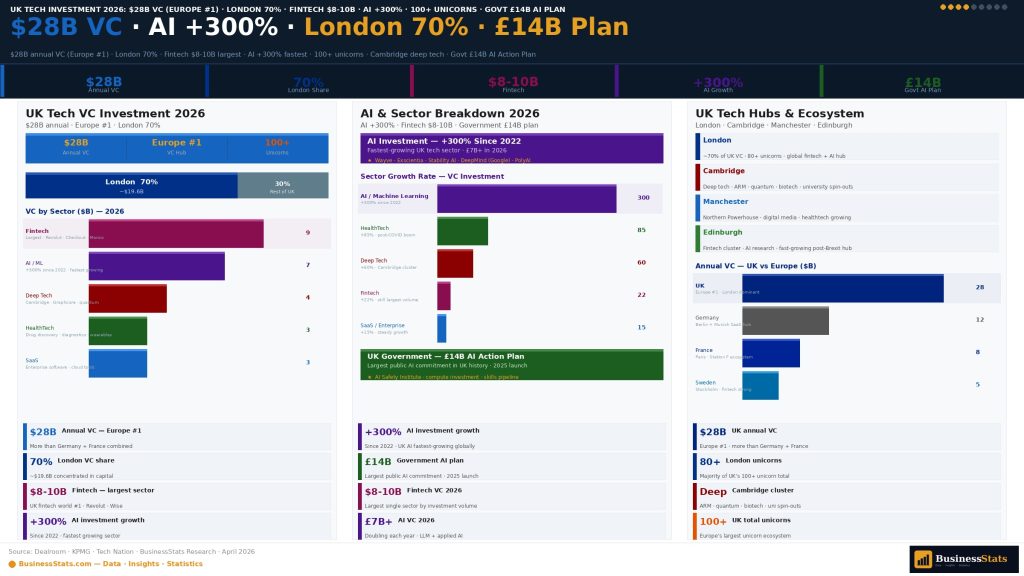

UK Tech Investment — $25–30B Annual VC, Europe's Largest Market

The UK received approximately $25–30 billion in venture capital and growth equity in 2025 — the 3rd largest VC market globally after the USA and China, and the largest in Europe. The UK consistently attracts more VC investment than France and Germany combined. London alone accounts for approximately 70% of all UK tech investment. Despite a global VC downturn in 2022–2023 (following the interest rate surge), UK tech investment has rebounded strongly in 2024–2025, driven by AI infrastructure deals and fintech growth rounds. The global investment landscape is analyzed in our financial markets analysis.

- UK total VC 2025: ~$28B · 3rd globally · 1st in Europe · London 70% share

- Largest UK deals 2025: Wayve ($1.05B, autonomous vehicles) · Abound ($800M, lending AI) · Synthesia ($90M, AI video) · multiple fintech growth rounds

- Investor concentration: SoftBank, Tiger Global, Sequoia Capital, Index Ventures, Accel are the most active UK tech investors

- AI investment surge: UK AI funding up ~300% since 2022 · government's £14B AI Action Plan adding to private capital

- Late-stage dominance: 60%+ of UK VC goes to Series B+ rounds — reflecting a mature ecosystem with fewer early-stage funding gaps

UK Tech Hubs — London and Beyond

While London dominates UK tech with approximately 70% of VC investment and 85% of unicorns, the UK has a genuinely national tech ecosystem with significant clusters outside the capital. Cambridge is the global heartland of deep tech — ARM, Darktrace, Featurespace, and hundreds of University of Cambridge spinouts call it home. The UK's tech hub diversity, including cities like Manchester, Edinburgh, and Bristol, creates regional economic growth tracked alongside global trends in our wealth and demographics analysis.

- London: ~70% of UK VC · Silicon Roundabout (Old St/Shoreditch) · King's Cross tech campus (Google, Meta, DeepMind) · Canary Wharf fintech · 500,000+ tech workers

- Cambridge: ARM, Darktrace, Graphcore, Featurespace · "Silicon Fen" · University spinout capital of Europe · deep tech and semiconductors

- Manchester: Rapidly growing fintech and digital media hub · MediaCityUK (BBC, ITV, dock10) · ~100,000 tech workers

- Edinburgh: Strong in fintech, data science, and games · Rockstar North (GTA) · Skyscanner founded here · 50,000+ tech workers

- Bristol: Graphcore HQ · strong in aerospace tech, robotics, semiconductors · University of Bristol spinout ecosystem

- Oxford: Oxford Nanopore Technologies · BioTech and HealthTech cluster · University spinout pipeline

- Belfast: Kainos HQ · growing cybersecurity cluster · cost-effective tech talent vs London · fintech growing

UK Tech Companies — Key Statistics & Facts 2026

Frequently Asked Questions — UK Tech Companies 2026

The UK technology sector is valued at approximately $1 trillion, making it the 3rd largest tech ecosystem in the world after the USA and China. The UK digital economy contributes approximately £150 billion (~$190B) to GDP annually — about 7.7% of total UK GDP. The tech sector employs approximately 3 million people directly and supports a further 2 million in adjacent roles. The UK has the largest tech sector in Europe, ahead of Germany and France.

The United Kingdom has approximately 100–110 technology unicorns (private companies valued at $1 billion+) as of early 2026, making it the 3rd largest unicorn ecosystem globally after the USA and China, and the largest in Europe. London alone accounts for approximately 85–90 of these. Notable UK unicorns: Revolut ($45B), Checkout.com ($11B), Snyk ($7.4B), Monzo ($5B), Octopus Energy ($5B), OakNorth ($2.8B), Thought Machine ($2.7B), Graphcore ($2.77B).

ARM Holdings (Cambridge) is the UK's largest publicly traded technology company, with a market capitalisation of approximately $100–120 billion after its Nasdaq re-listing in September 2023. ARM designs processor architectures used in approximately 99% of the world's smartphones. Among privately held companies, Revolut is the UK's most valuable tech startup at approximately $45 billion. Among UK FTSE-listed companies by revenue, Sage Group (~£2.2B revenue, £12B market cap) leads among pure-play tech.

The UK received approximately $25–30 billion in venture capital and growth equity in 2025, making it the 3rd largest VC market globally after the USA and China, and the largest in Europe. London accounts for approximately 70% of UK tech VC. The UK attracts more VC investment than France and Germany combined. Fintech is consistently the largest sector (~25–30% of total). The UK government's £14B AI Action Plan (2025) has additionally mobilised private capital.

Yes — London is widely recognised as Europe's leading technology hub by every major metric: most unicorns, most VC investment, most tech IPOs, most major tech company offices, highest concentration of AI researchers, and the continent's largest fintech cluster. Key London tech districts: Silicon Roundabout (Old Street/Shoreditch), King's Cross tech campus (Google, Meta, DeepMind, YouTube), Canary Wharf fintech corridor, and the South Bank. London employs approximately 500,000+ tech workers.

Largest UK tech sectors by VC investment and economic contribution: Fintech (~$8–10B VC/year) — Revolut, Wise, Monzo, Starling; AI/ML (~$6–8B) — DeepMind, Wayve, Graphcore, Stability AI; Cybersecurity (~$2–3B) — Darktrace, Snyk, Sophos; SaaS/Enterprise (~$3B) — Sage, Kainos; Gaming (~£3.4B revenue) — Rockstar, Codemasters, Frontier; GreenTech (~$3B+) — Octopus Energy; HealthTech (~$2B). AI is the fastest-growing sector (+300% since 2022).

The UK fintech sector generated approximately £11 billion in revenue in 2025 and employs approximately 76,000 people. The UK has the largest fintech sector in Europe and 2nd largest globally after the USA. London processes approximately 40% of all European fintech transactions. Major UK fintechs: Revolut ($45B), Wise ($9B, public), Checkout.com ($11B), Monzo ($5B), Starling Bank ($3.3B), OakNorth ($2.8B). The FCA's regulatory sandbox (launched 2016) has tested 800+ fintech firms and is widely credited with making the UK fintech-friendly.

The UK tech sector employs approximately 3 million people directly — approximately 9% of the total UK workforce. London accounts for approximately 35–40% of UK tech employment (~500,000+ workers). The average tech salary is approximately £55,000 — about 40% above the UK national average. Tech employment grew approximately 40% between 2015 and 2025. The UK faces a significant skills shortage with approximately 173,000 unfilled tech vacancies at any given time. Top in-demand skills: software development, data science, cybersecurity, cloud architecture, and AI/ML engineering.

ARM Holdings is a Cambridge-based company that designs processor architectures licensed to chipmakers worldwide. ARM's designs are used in approximately 99% of smartphones globally — including Apple iPhones (A-series, M-series), Samsung Galaxy (Exynos), and all Qualcomm Snapdragon devices. ARM was founded in 1990, acquired by SoftBank in 2016 for $32 billion, and re-listed on Nasdaq in September 2023, now valued at approximately $100–120 billion. ARM is considered the most strategically important technology company in the UK and a cornerstone of the global semiconductor industry.

DeepMind is a London-based AI research company founded in 2010 and acquired by Google (Alphabet) in 2014 for approximately $500 million. Major achievements: AlphaGo (2016, first AI to beat a world Go champion); AlphaFold (2020/21, solved the 50-year protein folding problem, described as the decade's biggest scientific breakthrough); AlphaZero (mastered chess, shogi, Go from scratch); co-developed Gemini AI models with Google Brain. DeepMind employs over 3,000 researchers, with headquarters at King's Cross, London. It is widely considered the world's leading AI research organisation.

The UK AI sector contributes approximately £3.7 billion to the UK economy directly, with the broader AI-enabled industry worth approximately £20 billion. The UK has the 3rd highest AI research output globally. The UK Government's AI Opportunities Action Plan (2025) mobilised £14 billion in private AI investment commitments. Key UK AI companies: DeepMind (Alphabet, London), Wayve (autonomous driving, $1B+), Graphcore (AI chips, $2.77B), Stability AI (generative AI), PolyAI (voice AI), and numerous AI-first startups. AI investment grew ~300% since 2022.

Brexit has had mixed effects. Negative impacts: reduced access to EU tech talent (EU workers now require visas); some companies relocated EU HQs to Amsterdam, Dublin, or Paris; initial loss of Horizon Europe funding (UK re-joined in 2024); and increased operational complexity for UK-EU tech businesses. Positive aspects: UK retained regulatory flexibility — particularly in AI, crypto, and financial services; the Global Talent Visa attracted international tech talent; and London has maintained its #1 European tech hub position throughout. Overall, UK tech has continued to grow strongly post-Brexit, though talent recruitment costs have increased.

Major UK tech companies on public markets: ARM Holdings (Nasdaq, ~$110B); Sage Group (LSE/FTSE 100, ~£12B, accounting software); Wise (LSE, ~£9B, fintech); Darktrace (LSE, ~£3B, AI cybersecurity); Softcat (LSE, ~£3.5B, IT infrastructure); Computacenter (LSE, ~£3B, IT services); Kainos (LSE, ~£1B, digital services); Bytes Technology (LSE, ~£1.5B). Notably, many UK tech successes list in New York rather than London due to higher valuation multiples — a structural challenge for the LSE.

Fastest growing UK tech sectors 2025/26: Generative AI — investment up ~300% since 2022; GreenTech/CleanTech — £3B+ invested in 2025; Cybersecurity — growing 15% annually; Quantum computing — UK has Europe's largest quantum programme; Space tech — UK targets 10% of global space market by 2030; Defence tech — increased NATO spending driving demand; HealthTech — AI diagnostics, drug discovery; Autonomous vehicles — Wayve ($1B+ from NVIDIA, SoftBank) leading globally in urban AV AI.

The UK video games industry generated approximately £3.4 billion in revenue in 2025 — the largest in Europe and 5th globally. Approximately 25,000 people work in UK game development. Major UK game studios: Rockstar North (Edinburgh, GTA series), Codemasters (Warwickshire, F1 series), Frontier Developments (Cambridge), Team17 (Wakefield), Jagex (Cambridge, RuneScape). The UK created some of gaming's most iconic franchises: Grand Theft Auto, Tomb Raider, Wipeout, Elite, and Lara Croft all originated in the UK. Total gaming economic contribution including indirect effects: approximately £10 billion.

Primary: KPMG Venture Pulse Q4 2025 — UK and European VC investment data, deal counts, sector analysis

Supporting: Tech Nation — UK Tech Ecosystem Report · Employment, hubs, skills, diversity, and growth data