Medical Technology Industry — $603 Billion in 2026

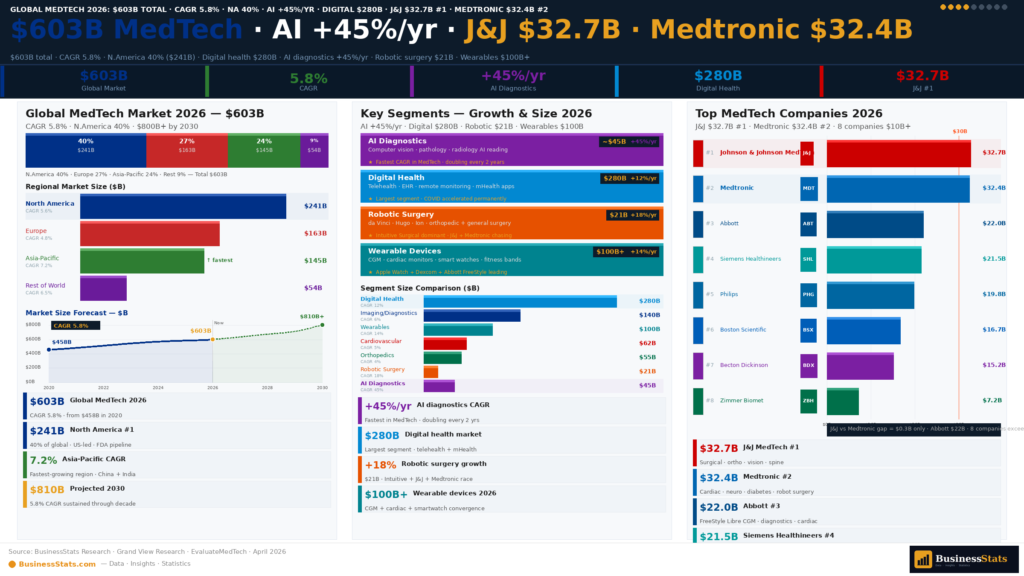

The global medical technology (MedTech) industry reached approximately $603 billion in 2026, growing at 5.8% annually — well above the broader healthcare sector's average growth rate. MedTech encompasses medical devices, diagnostic equipment, in-vitro diagnostics, digital health platforms, surgical robotics, and AI-powered clinical tools. The industry is experiencing its most transformative decade in history, driven by three converging forces: an aging global population creating unprecedented demand for chronic disease management and surgical interventions; artificial intelligence automating diagnostics and enabling precision medicine; and a post-pandemic digital health revolution that has permanently shifted care delivery toward remote monitoring, telehealth, and connected devices. The U.S. alone spends approximately $4.9 trillion annually on healthcare — a context covered in our U.S. financial markets analysis.

- Global market: ~$603B in 2026 · CAGR 5.8% · projected $780B by 2030

- Regional split: North America 40% ($241B) · Europe 28% ($169B) · Asia-Pacific 24% ($145B) · RoW 8%

- Fastest growing region: Asia-Pacific at 8.2% CAGR — China, India, South Korea driving volume

- AI in healthcare: $45B in 2026, growing 45% annually — fastest segment in all of MedTech

- R&D intensity: Industry spends ~$35–40B annually on R&D (~6–7% of revenue)

- Employment: ~700,000 direct MedTech jobs in the U.S. alone · 2M+ globally

The MedTech industry's fundamental value proposition has evolved. Where once a "medical device" was a surgical instrument or diagnostic machine, the category now spans smartphone-connected insulin pumps, AI algorithms that detect cancer in radiology scans faster than radiologists, exoskeletons for stroke rehabilitation, and smart contact lenses for continuous glucose monitoring. This blurring of the boundary between technology, software, and healthcare device has attracted the world's largest technology companies — Amazon, Apple, Google, and Microsoft all now have significant healthcare technology divisions. Amazon's health strategy is tracked in our Amazon statistics report.

- Apple Watch Health: ECG, blood oxygen, fall detection, atrial fibrillation alerts — FDA-cleared features on 50M+ active devices

- Amazon Health: Amazon Clinic, Amazon Pharmacy, One Medical acquisition ($3.9B) — building healthcare delivery ecosystem

- Google Health / DeepMind: AlphaFold protein structure prediction · Streams EHR platform · AI diabetic retinopathy detection

- Microsoft Healthcare: Azure Health Data Services · Nuance (DAX ambient clinical documentation) · $19.7B healthcare AI investments

Top Medical Technology Companies — Revenue Rankings 2025

Johnson & Johnson MedTech is the world's largest medical technology business by segment revenue, generating approximately $32.7 billion in 2025 following its separation from the consumer health business (Kenvue). J&J MedTech's portfolio spans orthopedic reconstruction (DePuy Synthes), surgical robotics (Ottava), cardiovascular (Abiomed), and eye health (AMO). Medtronic — the largest dedicated (pure-play) MedTech company — generated approximately $32.4 billion in fiscal year 2025, operating across cardiovascular ($12.8B), neuroscience ($8B), medical surgical ($8.1B), and diabetes ($3.5B). Both companies are closely tracked in our global market capitalization rankings.

- J&J MedTech (#1): $32.7B · Orthopedics, Surgical Vision, Cardiovascular, Surgical Robotics (Ottava)

- Medtronic (#2): $32.4B · Cardiovascular $12.8B · Neuroscience $8B · Medical Surgical $8.1B · Diabetes $3.5B

- Siemens Healthineers (#3): $23.7B · Diagnostic Imaging, Advanced Therapies, Atellica IVD solutions

- Abbott Laboratories (#4): ~$21B MedTech · FreeStyle Libre CGM · Alinity IVD · Structural Heart

- GE Healthcare (#5): $19.6B · MRI, CT, Ultrasound, Patient Monitoring, AI imaging solutions

- Philips Healthcare (#6): $18.2B · Diagnostic Imaging, Patient Monitoring, Connected Care, Sleep & Respiratory

- Stryker (#7): $21.4B · Orthopedics $9.0B · MedSurg $8.7B · Neurotechnology $3.7B

- Becton Dickinson (#8): $19.8B · BD Medical $10.2B · BD Diagnostics $5.3B · BD Life Sciences $4.3B

Siemens Healthineers — spun off from Siemens AG in 2018 and partially IPO'd — has emerged as the undisputed leader in diagnostic imaging and in-vitro diagnostics with $23.7 billion in revenue. Its acquisition of Varian Medical Systems ($16.4 billion, 2021) made it a major force in oncology radiation therapy — a strategic bet on the cancer treatment equipment market growing faster than traditional imaging. Abbott's FreeStyle Libre has become one of the most commercially successful MedTech products of the 2020s — its continuous glucose monitor (CGM) now commands approximately 60% of the global CGM market and generated approximately $5.3 billion in revenue in 2025 alone. The CGM market disruption exemplifies how MedTech creates entirely new care paradigms. Consumer health technology trends are tracked in our global company rankings.

Top 10 MedTech Companies — Global Revenue 2025 (USD Billion)

The navy bar chart below ranks the top 10 MedTech companies by 2025 revenue. Hover each bar to see the exact figure. J&J MedTech and Medtronic are near-equal at the top — separated by just $300 million.

Top 15 MedTech Companies — Sortable Rankings Table 2025

Click any column to sort. All revenues in USD at approximate 2025 exchange rates from company annual reports.

| Rank | Company | Revenue (USD) | YoY Growth | Key Segment | HQ |

|---|---|---|---|---|---|

| 1 | J&J MedTech | $32.7B | +4.8% | Orthopedics, Surgical Robotics | New Brunswick, NJ |

| 2 | Medtronic | $32.4B | +3.1% | Cardiovascular, Neuroscience | Dublin / Minneapolis |

| 3 | Stryker | $21.4B | +8.9% | Orthopedics, MedSurg, Neurotech | Kalamazoo, MI |

| 4 | Abbott Laboratories | ~$21.0B | +6.2% | FreeStyle Libre CGM, IVD, Structural Heart | Abbott Park, IL |

| 5 | Siemens Healthineers | $23.7B | +7.5% | Diagnostic Imaging, IVD, Oncology | Erlangen, Germany |

| 6 | Becton Dickinson (BD) | $19.8B | +4.2% | Medical Devices, Diagnostics, Life Sciences | Franklin Lakes, NJ |

| 7 | GE Healthcare | $19.6B | +5.8% | Imaging (MRI/CT/US), Patient Monitoring | Chicago, IL |

| 8 | Philips Healthcare | $18.2B | +2.8% | Imaging, Patient Care, Sleep & Respiratory | Amsterdam, Netherlands |

| 9 | Boston Scientific | $16.7B | +11.2% | Cardiology, Electrophysiology, Endoscopy | Marlborough, MA |

| 10 | Zimmer Biomet | $7.8B | +5.4% | Joint Reconstruction (Knee/Hip) | Warsaw, IN |

| 11 | Intuitive Surgical | $8.4B | +14.0% | da Vinci Robotic Surgery System | Sunnyvale, CA |

| 12 | Danaher (MedTech) | $15.6B | +3.5% | Diagnostics, Life Science Tools | Washington D.C. |

| 13 | Edwards Lifesciences | $6.7B | +9.1% | TAVR Heart Valves, Critical Care | Irvine, CA |

| 14 | Smith+Nephew | $5.4B | +4.8% | Orthopedics, Sports Medicine, Wound | London, UK |

| 15 | Hologic | $3.9B | +3.2% | Women's Health, Diagnostics, Breast Health | Marlborough, MA |

While the MedTech industry average growth is 5.8%, Boston Scientific achieved +11.2% revenue growth in 2025 — nearly double the industry rate — reaching $16.7 billion. The company's strategic focus on high-growth electrophysiology (cardiac arrhythmia ablation) has proven prescient: its FARAPULSE pulsed field ablation (PFA) system became the fastest product launch in the company's history, capturing significant market share from older thermal ablation technologies. Similarly, Intuitive Surgical (+14.0%) is benefiting from rapid da Vinci system installation growth in Asia-Pacific, particularly Japan, China, and South Korea. Meanwhile, Philips continues its slowest growth period (+2.8%) as it works through the massive CPAP recall (2021–2024) that affected over 10 million ventilators and respiratory devices worldwide. The global company rankings and valuations context is covered in our most valuable companies analysis.

MedTech Market Share by Region 2026 (Donut)

North America's 40% share reflects the U.S. healthcare system's premium pricing and high device adoption rates. Asia-Pacific at 24% is growing fastest — China alone is expected to become the world's second-largest MedTech market by 2028.

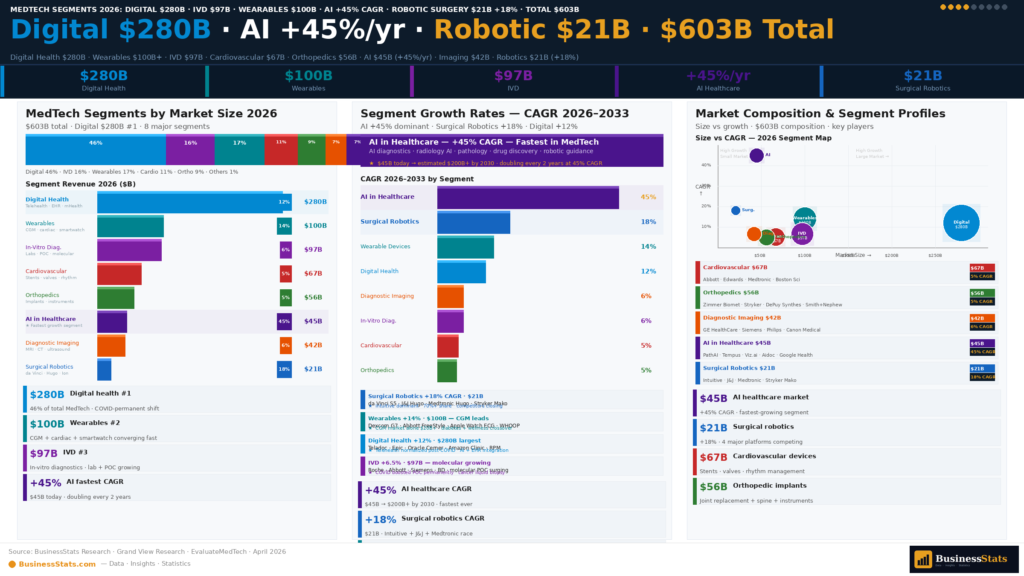

MedTech Market Segments — Cardiovascular, Orthopedics, Diagnostics & More

The MedTech market is organized into distinct clinical segments, each with its own growth drivers, competitive dynamics, and technology trajectories. Cardiovascular devices are the largest segment at approximately $67 billion — reflecting the global burden of heart disease as the world's leading cause of death. The segment spans everything from coronary stents and heart valves to implantable defibrillators, pacemakers, and the rapidly growing transcatheter aortic valve replacement (TAVR) technology pioneered by Edwards Lifesciences. In-vitro diagnostics (IVD) — laboratory testing — is the second-largest at $97 billion, boosted permanently by the COVID-19 testing infrastructure investments of 2020–2022. Country-level healthcare spending patterns are analyzed in our global GDP analysis.

- In-Vitro Diagnostics (IVD): $97B — lab testing, POC diagnostics, molecular testing, immunoassays

- Cardiovascular Devices: $67B — stents, valves, pacemakers, defibrillators, TAVR, EP ablation

- Digital Health: $280B — telehealth $85B, remote monitoring $35B, digital therapeutics $8B, health apps

- Orthopedic Devices: $56B — joint reconstruction $24B, spine $11B, sports medicine $8B, trauma $7B

- Diagnostic Imaging: $42B — MRI $12B, CT $11B, ultrasound $9B, X-ray $8B, nuclear medicine $2B

- Wearable Medical Devices: $100B+ — CGMs, cardiac monitors, fitness/health wearables, smart implants

- Surgical Robotics: $21B — da Vinci (Intuitive), Hugo (Medtronic), Ottava (J&J), Ion (Intuitive, lung biopsy)

- AI in Healthcare: $45B — radiology AI, pathology AI, clinical decision support, drug discovery AI

MedTech — Market Size by Segment 2026 (USD Billion)

The AUV bars below show segment size. Digital health's $280B makes it the largest umbrella category — but note it overlaps with traditional MedTech segments (e.g., connected devices) and extends into software and services beyond hardware devices.

MedTech Segment Growth Rates — CAGR 2024–2030

The grouped bar chart compares annual growth rates across MedTech segments. AI diagnostics (+45%) stands dramatically apart — representing the technology disruption layer being applied across all traditional MedTech categories simultaneously.

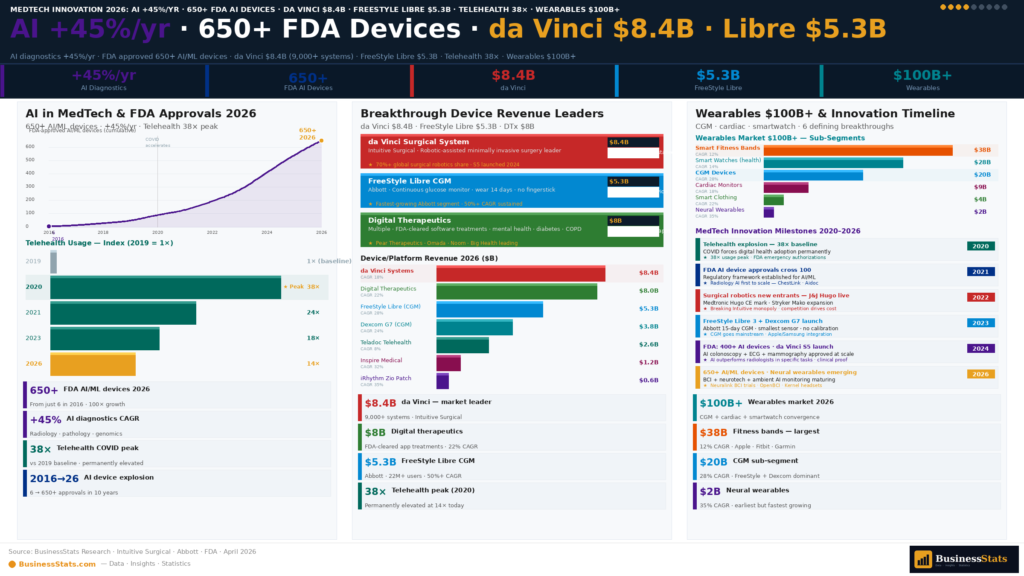

AI in Healthcare & Digital Health — The $280 Billion Transformation

Artificial intelligence is the most disruptive force in MedTech history — not because it replaces devices, but because it dramatically amplifies their value. AI-powered radiology can detect lung nodules, diabetic retinopathy, and early breast cancer with sensitivity comparable to — and in some studies exceeding — specialist radiologists. The FDA has approved over 650 AI/ML-based medical devices through 2025, up from just 6 in 2015 — a 100× acceleration in regulatory approvals in a decade. The AI healthcare market reached approximately $45 billion in 2026 and is growing at 45% annually — the single fastest-growing technology segment in healthcare. The broader technology company investments in this space are tracked in our Amazon health statistics and global company valuations.

- FDA AI/ML device approvals: 6 (2015) → 650+ (2025) — 100× growth in 10 years

- AI radiology market: ~$2.8B in 2026 · growing 35% p.a. · Aidoc, Arterys, Zebra Medical leading

- AI pathology: Paige.AI, PathAI — digital pathology + AI detecting cancer in tissue biopsies

- AI drug discovery: Insilico Medicine, Recursion Pharmaceuticals — AI designed drugs entering Phase 2 trials

- DeepMind AlphaFold: Predicted structure of 200M+ proteins — fundamentally accelerating drug target discovery

- Clinical decision support: Epic's AI models, IBM Watson Health successors — reducing diagnostic errors by 35–50%

Digital health — the $280 billion category encompassing telehealth, health apps, remote patient monitoring, digital therapeutics, and connected health platforms — has undergone a permanent structural transformation since COVID-19. Telehealth visits reached 38× pre-pandemic levels in peak periods and have stabilized at approximately 5–8× pre-pandemic baseline — meaning the digital health revolution is not a temporary pandemic artifact but a new healthcare delivery paradigm. The U.S. mental health app market alone — where digital therapeutics like Calm, Headspace, and BetterHelp operate — reached approximately $6.2 billion in 2026. Social media's role in digital health awareness and patient communities is tracked in our social media statistics and Instagram analysis.

- Telehealth market: ~$85B in 2026 · growing 18% p.a. · Teladoc, MDLive, Amwell leading

- Remote patient monitoring (RPM): ~$35B · growing 28% p.a. · heart failure, diabetes, hypertension focus

- Digital therapeutics (DTx): ~$8B · FDA-authorized prescription apps treating depression, diabetes, ADHD, substance abuse

- Mental health apps: ~$6.2B · Calm $100M+ ARR · BetterHelp (Teladoc) $1.1B revenue · Headspace $100M+ ARR

- Rock Health funding: Digital health startups raised $10.1B in 2025 — recovery from 2022/23 funding winter

Surgical Robotics & Wearable Medical Devices

Intuitive Surgical's da Vinci system remains the dominant force in surgical robotics — but its monopoly is genuinely under threat for the first time. With approximately 9,000 installed systems globally and over 2.5 million procedures performed annually, da Vinci generated approximately $8.4 billion in revenue in 2025 (+14%). However, Johnson & Johnson's Ottava system received CE Mark approval in Europe in 2025 and is expected to receive FDA clearance in 2026. Medtronic's Hugo RAS system is already commercially available in multiple countries. The surgical robotics market grew 18% annually to approximately $21 billion in 2026 — with orthopedic robotics (Stryker Mako, Zimmer Rosa) growing even faster as computer-assisted joint replacement becomes standard of care.

- Intuitive Surgical da Vinci: $8.4B revenue · 9,000+ installed systems · 2.5M+ procedures/yr · 75%+ market share

- J&J Ottava: CE Mark 2025 · FDA pending 2026 · targeting general surgery, gynecology, urology

- Medtronic Hugo: Commercially available in Europe, Asia · soft tissue surgical robotics

- Stryker Mako: #1 robotic joint replacement · 1,800+ installations · partial/total knee and hip

- Intuitive Ion: Robotic-assisted bronchoscopy for peripheral lung biopsy — growing 80%+ p.a.

- Orthopedic robotics total: ~$3.2B in 2026 · growing 25% annually · Stryker Mako dominant

Wearable medical devices have crossed $100 billion in 2026 — driven by the convergence of consumer electronics, clinical-grade biosensors, and FDA clearances for smartwatch health features. Abbott's FreeStyle Libre and Dexcom's G7 CGM systems have transformed diabetes management — the CGM market alone reached approximately $8.2 billion in 2026, growing 31% annually. Apple Watch's expanding health feature set — FDA-cleared ECG, atrial fibrillation detection, fall detection, irregular rhythm notifications, and crash detection — makes it the world's most widely deployed "medical device" by units, with approximately 50 million active Apple Watches carrying clinically validated health monitoring. The consumer health technology overlap with broader tech company strategies is tracked in our global market cap report.

Medical Technology Industry — Key Statistics & Facts 2026

MedTech Market Forecast & Outlook 2026–2030

The global MedTech market is projected to reach approximately $780 billion by 2030 at a CAGR of 5.8–6.5%. Four structural megatrends power this forecast and are accelerating simultaneously. Global healthcare economics are analyzed in our global GDP report, which shows healthcare's rising share of GDP across all major economies.

- Aging demographics: Global population aged 65+ projected to reach 1.5 billion by 2030 — driving orthopedic, cardiovascular, and neurology device demand

- AI integration: Every traditional MedTech segment is adding AI layers — imaging AI, robotics AI, wearable AI — creating 45%+ growth in AI healthcare sub-segments

- Emerging market expansion: China, India, Brazil, Indonesia — rapidly expanding hospital infrastructure + growing middle class demanding advanced devices

- Combination products: MedTech + biotech convergence — drug-eluting stents, drug delivery devices, gene therapy delivery — creating new high-value product categories

Key risks to the forecast include regulatory complexity (EU MDR implementation has increased compliance costs dramatically), supply chain vulnerabilities exposed by COVID-19 (many critical components sourced from single countries), and reimbursement pressure as payers globally push back on premium device pricing. The talent war for AI/ML engineers and data scientists is also creating execution risk for traditional MedTech companies attempting digital transformation. The broader wealth distribution patterns that affect healthcare access and insurance coverage — which directly impact MedTech adoption — are tracked in our U.S. wealth statistics.

- Risk — EU MDR: EU Medical Device Regulation dramatically increased clinical evidence requirements · many SME manufacturers exiting European market

- Risk — China localization: China pushing domestic MedTech (Mindray, United Imaging) over foreign devices — pressure on Western incumbents in the world's fastest-growing market

- Upside — CGM disruption: Apple Watch rumored glucose monitoring · could add 500M+ new CGM users instantly

- Upside — AI regulatory acceleration: FDA's AI/ML action plan streamlining approvals — could unlock $50B+ in new AI MedTech faster than projected

- Upside — GLP-1 synergy: Ozempic/Wegovy obesity drug success paradoxically boosting cardiac device demand (heart failure management) while pressuring diabetes device volumes

Frequently Asked Questions — Medical Technology Industry 2026

The global medical technology (MedTech) market reached approximately $603 billion in 2026, growing at a CAGR of 5.8%. It is projected to reach approximately $780 billion by 2030. The market encompasses medical devices, diagnostic imaging, in-vitro diagnostics, digital health platforms, surgical robotics, and AI-powered healthcare solutions. North America accounts for approximately 40% of global value ($241B), followed by Europe (28%, $169B), and Asia-Pacific (24%, $145B). Asia-Pacific is the fastest-growing region at 8.2% CAGR, driven by healthcare infrastructure expansion in China, India, and South Korea.

Johnson & Johnson MedTech is the world's largest medical technology business by segment revenue, generating approximately $32.7 billion in 2025. Medtronic is the largest dedicated (pure-play) MedTech company at approximately $32.4 billion. Siemens Healthineers ($23.7B), Stryker ($21.4B), Abbott ($21.0B), Becton Dickinson ($19.8B), GE Healthcare ($19.6B), and Philips Healthcare ($18.2B) round out the top tier. By market capitalization, Intuitive Surgical often trades at a premium valuation despite lower revenue due to its dominant robotic surgery market position.

AI-powered diagnostics is the fastest-growing segment in MedTech at approximately 45% annual growth. The broader AI in healthcare market reached approximately $45 billion in 2026 and is projected to reach $148 billion by 2029. At the device category level, wearable medical devices (+22% p.a.), remote patient monitoring (+28% p.a.), surgical robotics (+18% p.a.), and continuous glucose monitors (+31% p.a.) are the top growth segments. The FDA approved over 650 AI/ML-based medical devices by end of 2025, up from just 6 in 2015 — a 100× acceleration in a decade.

The global surgical robotics market reached approximately $21 billion in 2026, growing at 18% annually. Intuitive Surgical's da Vinci system dominates with approximately 75%+ market share, approximately 9,000 installed systems globally, and over 2.5 million robotic procedures performed annually. Revenue: $8.4 billion in 2025 (+14%). New competitors are entering: J&J's Ottava (CE Mark 2025, FDA 2026E), Medtronic's Hugo (commercially available in Europe), and orthopedic robotics (Stryker Mako, Zimmer Rosa for joint replacement). The market is projected to reach $45 billion by 2030.

The wearable medical devices market crossed $100 billion in 2026, growing at approximately 22% annually. Key segments: continuous glucose monitors (CGMs) — $8.2 billion growing 31% annually (Abbott FreeStyle Libre ~$5.3B, Dexcom ~$3.1B); cardiac monitoring wearables ($3.5B); and health-monitoring smartwatches (Apple Watch, Samsung Galaxy Watch, Garmin) now carrying FDA-cleared health features. Apple Watch has approximately 50 million active devices with clinically validated ECG, atrial fibrillation detection, fall detection, and irregular rhythm notifications — making it arguably the world's most widely deployed medical monitoring device by units.

The AI in healthcare market reached approximately $45 billion in 2026, growing at 45% annually — one of the fastest-growing technology segments globally. Key AI applications in MedTech include: medical imaging AI (radiology, pathology — Aidoc, Zebra Medical, Paige.AI); clinical decision support (Epic's AI models, reducing diagnostic errors); AI-powered drug discovery (Recursion Pharmaceuticals, Insilico Medicine — AI-designed drug candidates entering clinical trials); and genomics/precision medicine AI (Tempus, Foundation Medicine). The market is projected to reach $148 billion by 2029. The FDA had approved over 650 AI/ML medical devices by end 2025.

The U.S. medical technology market reached approximately $241 billion in 2026 — representing approximately 40% of global MedTech value. The U.S. is the world's largest single national MedTech market, driven by the world's highest per-capita healthcare spending (approximately $14,570 per person), a strong innovation culture, and favorable FDA regulatory pathways. Approximately 6,000+ MedTech companies operate in the U.S. Major MedTech industry clusters: Minneapolis-St. Paul (cardiac devices — Medtronic, Boston Scientific), San Diego (diagnostics), Boston/Cambridge (life sciences — Intuitive Surgical's base), and Silicon Valley (digital health/AI MedTech).

The digital health market reached approximately $280 billion in 2026, growing at 18% annually. Key sub-segments: telehealth (~$85B — Teladoc, MDLive, Amwell); remote patient monitoring (~$35B, +28% p.a.); digital therapeutics (~$8B — FDA-authorized prescription apps for diabetes, depression, ADHD); mental health apps (~$6.2B — BetterHelp, Calm, Headspace). COVID-19 permanently transformed telehealth adoption — monthly telehealth visits are approximately 5–8× pre-pandemic baseline levels in 2026, confirming digital health as a structural shift rather than a pandemic-era temporary trend. Digital health startups raised $10.1 billion in 2025.

Medtronic generated approximately $32.4 billion in revenue in fiscal year 2025 (ending April 30, 2025). It is the world's largest dedicated medical technology company, operating in four segments: Cardiovascular ($12.8B, 39%) — pacemakers, defibrillators, coronary stents, heart valves; Medical Surgical ($8.1B, 25%) — surgical instruments, patient monitoring, respiratory; Neuroscience ($8.0B, 25%) — brain stimulators, spinal cord stimulation, spine surgery; Diabetes ($3.5B, 11%) — insulin pumps, CGMs. Medtronic operates in 150+ countries, employs approximately 95,000 people, and invests approximately $2.7 billion annually in R&D.

Top MedTech trends in 2026: (1) AI diagnostics explosion — 45% annual growth, 650+ FDA-approved AI medical devices; (2) Surgical robotics competition — J&J Ottava and Medtronic Hugo challenging da Vinci's monopoly for the first time; (3) CGM mainstreaming — Abbott FreeStyle Libre and Dexcom growing 30%+ as CGM moves beyond insulin-dependent diabetes; (4) GLP-1 impact — Ozempic/Wegovy obesity drugs reshaping diabetes device demand; (5) Digital therapeutics regulatory maturation — FDA DTx pathways enabling prescription apps; (6) Point-of-care diagnostics — hospital-to-home testing expansion; (7) Augmented reality surgery — AR-guided surgical navigation entering mainstream use.

The global in-vitro diagnostics (IVD) market reached approximately $97 billion in 2026 — the largest traditional MedTech segment. IVD includes laboratory testing equipment, reagents, and analyzers used in clinical labs, hospitals, and at-home. The market surged during COVID-19 (reaching ~$110B in 2021 due to massive PCR/antigen test demand) before normalizing. Key companies: Roche Diagnostics (~$16B, global leader), Abbott (~$9B IVD, Alinity platform), Danaher/Cepheid (~$8B), Siemens Healthineers (~$6B IVD), bioMérieux (~$3.8B). Point-of-care testing is the fastest-growing IVD sub-segment, driven by post-COVID expansion of rapid at-home and bedside testing.

The global orthopedic devices market reached approximately $56 billion in 2026, growing at 4.8% annually. Key segments: joint reconstruction ($24B — knee and hip replacements, Zimmer Biomet, J&J DePuy Synthes, Stryker lead); spine ($11B — disc replacements, fusion devices, Medtronic dominant); sports medicine ($8B — ACL repair, shoulder reconstruction, Smith+Nephew); trauma ($7B — fracture fixation, DePuy Synthes leads); orthopedic biologics ($6B — bone grafts, PRP). The fastest-growing sub-segment is robotic joint replacement — Stryker Mako robotic system installations growing 25%+ annually, increasingly standard of care for partial and total knee replacement.

The global MedTech market is projected to reach approximately $780 billion by 2030, growing at a CAGR of 5.8–6.5%. Key growth drivers: aging global population (1.5B aged 65+ by 2030); AI integration across all MedTech segments; Asia-Pacific healthcare infrastructure expansion (Asia-Pacific projected to grow from 24% to ~35% of global market by 2030); and MedTech-biotech convergence (combination drug-device products). The AI healthcare sub-market alone is projected to reach $148 billion by 2029. Wearable medical devices are projected to reach $180 billion by 2030 as consumer devices gain more clinical-grade health monitoring features.

The GLP-1 drug boom (Ozempic, Wegovy, Mounjaro/Tirzepatide) is having a complex, nuanced impact on MedTech. Negative near-term effects: Bariatric surgery device demand declining (Intuitive Surgical, J&J Ethicon seeing procedure slowdowns); diabetes device volumes under pressure as better blood sugar control reduces continuous monitoring need for some patients; knee replacement procedures may slow as obesity-driven joint damage is reduced. Positive long-term effects: GLP-1 drugs dramatically reduce cardiovascular events — but heart failure patients who survive longer still need cardiac devices (pacemakers, defibrillators); obesity reduction improving surgical outcomes, expanding the eligible surgical population. Net consensus: GLP-1 drugs are a modest headwind for diabetes MedTech but a long-term tailwind for cardiovascular devices.

The global MedTech industry spends approximately $35–40 billion annually on R&D — approximately 6–7% of total industry revenue. This is above most manufacturing sectors (automotive ~4%, aerospace ~5%) but below pharmaceuticals (~15%). Top individual company R&D spenders: J&J MedTech (~$3.5B), Medtronic (~$2.7B), Abbott ($2.4B), Siemens Healthineers ($2.1B), GE Healthcare ($1.9B), Stryker ($1.5B). The FDA approved approximately 65 novel de novo medical devices and 47 PMA novel devices in 2025. MedTech's R&D-to-revenue cycle is typically 5–10 years from initial concept to market — significantly shorter than pharmaceuticals (10–15 years).